TRY OUR GROWTH SCANNER

Venture Capital Benchmark Q1 2026

US, Europe, and Latin America

VC Activity

Q1 2026 opened with a historic split between value and volume. Global deal count fell 27% compared to Q1 2025, continuing the trend of investors concentrating capital into fewer, larger bets across all regions. Yet total deal value told the opposite story, surging to $330.8B globally, with North America alone hitting $268.5B, more than 6x what it deployed in Q1 2025. North America captured 81% of global VC investment this Q1, a concentration level without precedent. Strip out the frontier lab megarounds and the underlying market remains cautious, but the headline numbers mark a structural shift in how and where capital is being deployed.

Early 2026 fundraising signals a cautious rebound after a difficult 2025. Global VC raised fell 41% in 2025 (from $217.8B in 2024 to $128.8B), continuing a multi-year contraction. Q1 2026 already shows $58.3B raised — 45% of the entire 2025 total in a single quarter. Whether this marks a genuine recovery or is concentrated in a handful of large platforms will become clearer as the year progresses.

Global VC exit value surged 124% QoQ in Q1 2026 to $413.4B, driven overwhelmingly by North American mega-exits. Exit count, however, dropped 20% QoQ to 700 deals globally, continuing a sustained decline across all regions. The gap between value and volume tells the same story as dealmaking: liquidity is returning, but it is highly concentrated and not yet broad-based.

Source:pitchbook

01

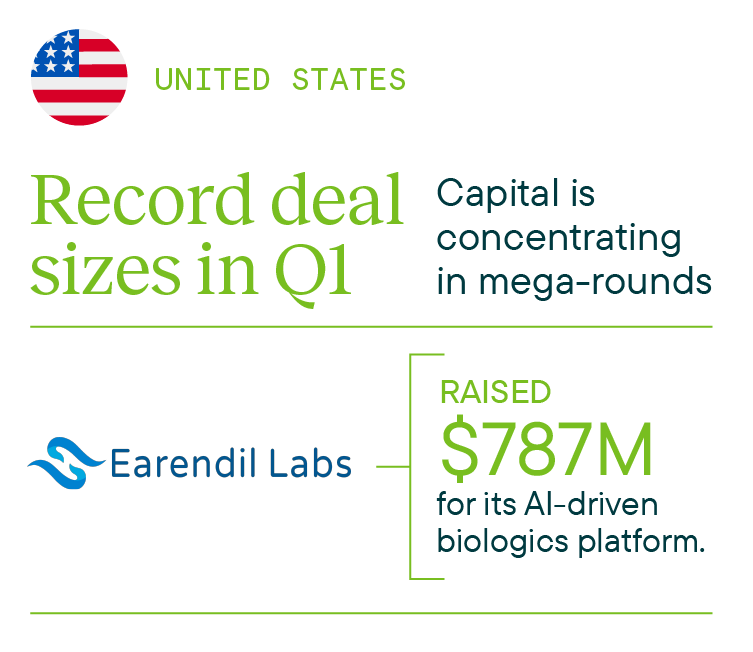

The rise of european mega-rounds

Q1 2026 has been defined by the emergence of "US-sized" mega-rounds in Europe. Investors are moving toward less saturated markets, leading to several record-breaking funding rounds:

Source:pitchbook

02

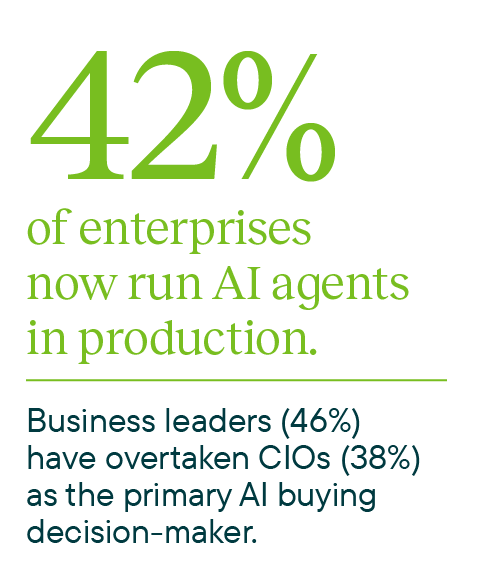

Agentic AI goes from pilot to production

Enterprise AI agents have crossed from experimentation to live workflows, and the revenue is following. Anthropic surpassed OpenAI in annualised revenue for the first time in Q1 2026, as enterprises turn agentic.

The open-source world accelerated the same shift, with new autonomous agent frameworks, like OpenClaw or Nanobot, becoming viral among developers, drawing endorsements from NVIDIA and prompting YCombinator to update its founding motto to “Make Something Agents Want”.

This is already playing out in our own portfolio: Simpliroute's ADA agents integrate directly with ERP, TMS, and WMS systems to autonomously resolve logistics incidents in real time. The new challenge is no longer convincing companies to try agents. It is scaling them without breaking things.

03

Revenue is now an engineering problem

The fastest-growing companies in Q1 aren't hiring bigger sales teams, they're engineering their GTM as a system. AI handles prospecting, qualification, outreach, and expansion. Founders with an engineering mindset are outbuilding those with a sales mindset.

04

Bioscience is back, and investors mean it this time

After years behind SaaS, and then AI, bioscience is rebounding in Q1 2026. The focus has shifted from diagnostic tools to owning the continuous patient relationship. In a market where AI is now baseline, the true asset for the patient is the ongoing data stream, not the one-time diagnosis. Capital is re-pricing accordingly.

Source:labiotech

Source:elsc / invest europe

Looking ahead

The IPO market gets its first real test

The models are commoditising

The rules for valuing AI companies are being rewritten

Ecosystem builder perspective

María Dancausa, product manager at TheVentureCity, describes our approach to building a GenAI product.

Rewind to this time last year, and the headlines were dark and ominous. They were ablaze with layoff news and economists fueling the fire with warnings of more turbulent times ahead. The questions on everyone’s mind: can the US pull off a soft landing while curbing inflation? How will quantitative tightening impact consumer spending? How will the technology ecosystem weather the storm?

A few things are clear in hindsight. In the public markets, investors enjoyed a strong end to the year, albeit after a bumpy start. The S&P ended 2023 at +24% and the tech-heavy Nasdaq at +43%. The magnificent seven, comprised of companies that already have some of the largest market cap, smashed it with a 111% YoY growth (Kiplinger). Within this power basket is NVIDIA, the stock everyone wishes they had bought in Q1 2023, which ended up an astonishing 239% over the full year of 2024 (Statista).

Last quarter we reported a brief opening of the IPO market. We remain confident that we will see more companies go public in the back half of 2024 and into 2025, and have noted hundreds of quality candidates detailed in CB Insights’ IPO pipeline of 250+ companies (CB Insights).

Bucking the downward B2C trend we mentioned earlier, Shopify, up 124% YoY, caught our attention. We have always leaned into the e-commerce enabler space, making notable investments such as in our very own Returnly, acquired by Affirm in 2021, so we are excited to see the momentum within this space.