TRY OUR GROWTH SCANNER

Venture Capital Benchmark Q4 2025

US, Europe, and Latin America

VC Activity

In Q4 2025, global VC deal volume declined across all regions, yet North America’s value surged 32% to 93.7 $B QoQ. While Europe’s deal value dropped by the same percentage, Asia and Latin America saw slight increases in value despite the overall reduction in total deal counts. Geographic concentration remains highly asymmetrical, with the U.S. leading both investment volume and deal size.

Q4 confirmed the continued slowdown in global VC fundraising in 2025, which plummeted 45% across all regions (from $219B in 2024 to $118B in 2025). The US still accounted for 57% of all global funds raised.

Global VC exit value surges 16% in Q4 driven by North American mega-rounds, despite the 10% drop in exit count.

Source:pitchbook

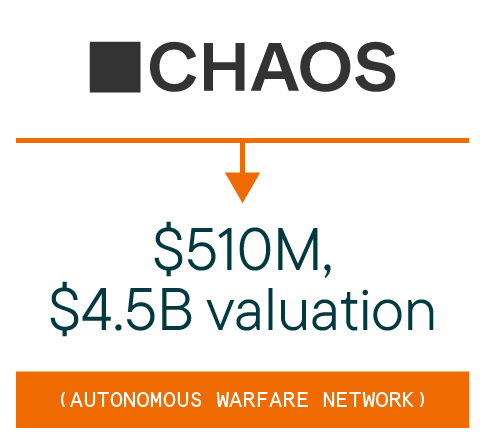

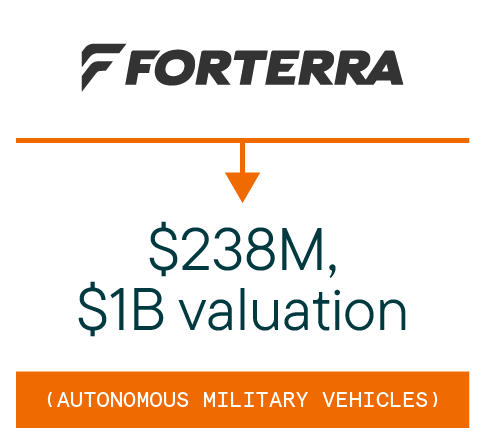

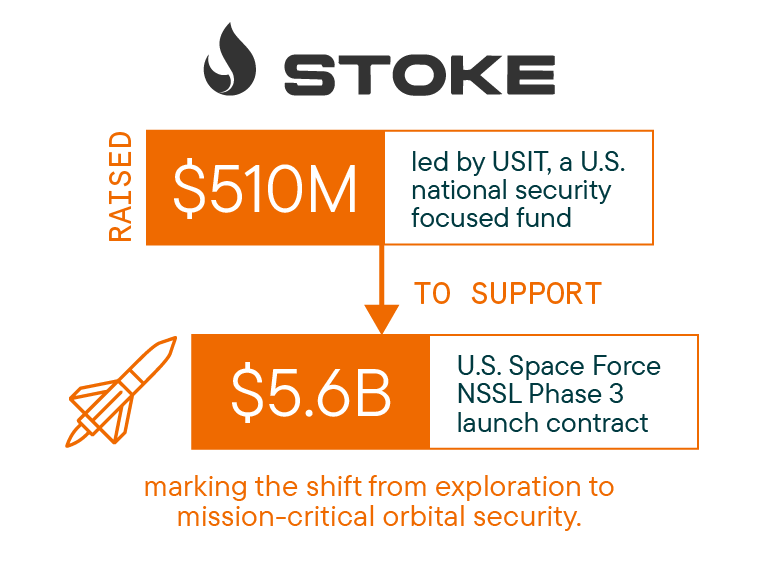

US Defense tech of critical infrastructure:

Q4 2025 marked a decisive shift as U.S. anchored defense and security technologies became a strategic priority, with capital flowing into companies directly tied to U.S. defense contracts, sovereign infrastructure, and autonomous warfare capabilities.

Core Defense & Autonomous Warfare:

Capital concentrated into scalable, kinetic defense capabilities, with megarounds on autonomous and weapons systems:

Q4 2025 marked a historic milestone for European healthtech

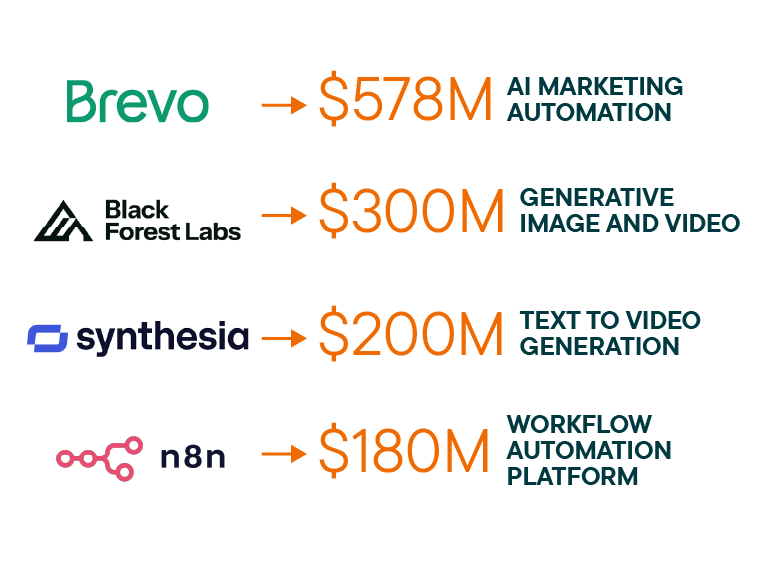

In Europe, earlier in the year investor attention centered on LLMs and AI infrastructure, but Q4 2025 showed VC investors increasingly prioritizing application layer solutions.

Looking ahead

Ecosystem builder perspective

María Dancausa, product manager at TheVentureCity, describes our approach to building a GenAI product.

Rewind to this time last year, and the headlines were dark and ominous. They were ablaze with layoff news and economists fueling the fire with warnings of more turbulent times ahead. The questions on everyone’s mind: can the US pull off a soft landing while curbing inflation? How will quantitative tightening impact consumer spending? How will the technology ecosystem weather the storm?

A few things are clear in hindsight. In the public markets, investors enjoyed a strong end to the year, albeit after a bumpy start. The S&P ended 2023 at +24% and the tech-heavy Nasdaq at +43%. The magnificent seven, comprised of companies that already have some of the largest market cap, smashed it with a 111% YoY growth (Kiplinger). Within this power basket is NVIDIA, the stock everyone wishes they had bought in Q1 2023, which ended up an astonishing 239% over the full year of 2024 (Statista).

Last quarter we reported a brief opening of the IPO market. We remain confident that we will see more companies go public in the back half of 2024 and into 2025, and have noted hundreds of quality candidates detailed in CB Insights’ IPO pipeline of 250+ companies (CB Insights).

Bucking the downward B2C trend we mentioned earlier, Shopify, up 124% YoY, caught our attention. We have always leaned into the e-commerce enabler space, making notable investments such as in our very own Returnly, acquired by Affirm in 2021, so we are excited to see the momentum within this space.