TRY OUR GROWTH SCANNER

Venture Capital Benchmark Q3 2025

US, Europe, and Latin America

VC Activity

Q3 maintained the strong deal values seen throughout 2025, even as overall deal volumes continued to decline. The surge in VC investment is largely driven by the increased activity in the US, as they remain the undisputed leader.

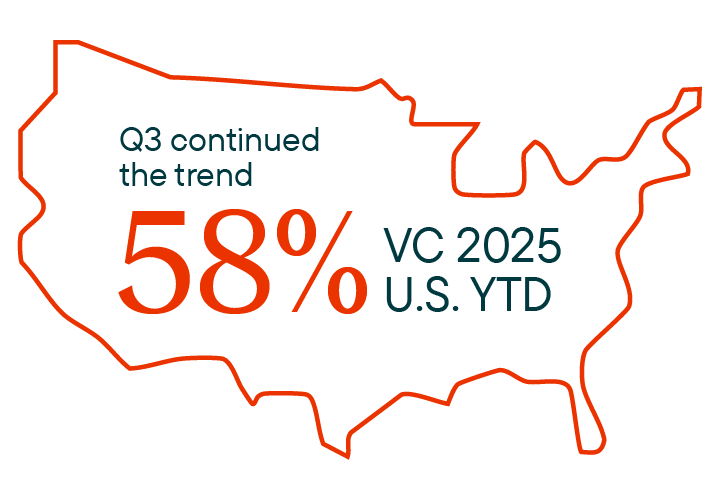

Q3 continued the trend of subdued VC fundraising in 2025, with the US still accounting for the majority of capital raised in 2025 YTD (58%).

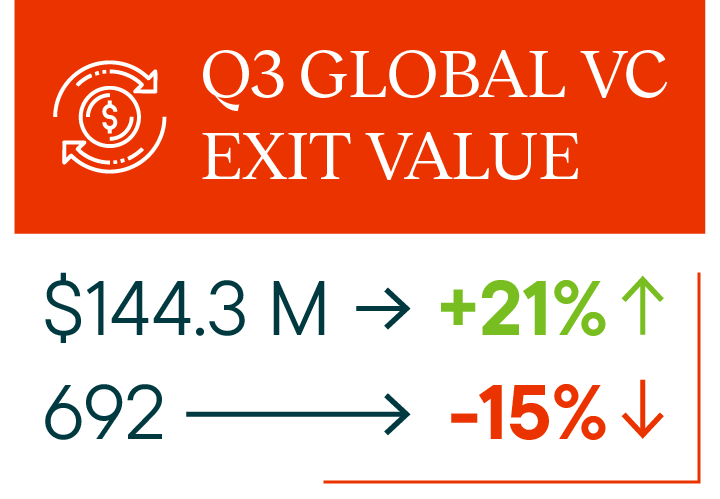

Global Quarterly VC Exit Value Surges in Q3 Despite Decline in Exit Count.

Note for all metrics above: Mexico is included in Latin America, not North America.

Source for all VC activity: Pitchbook

M&A Trends

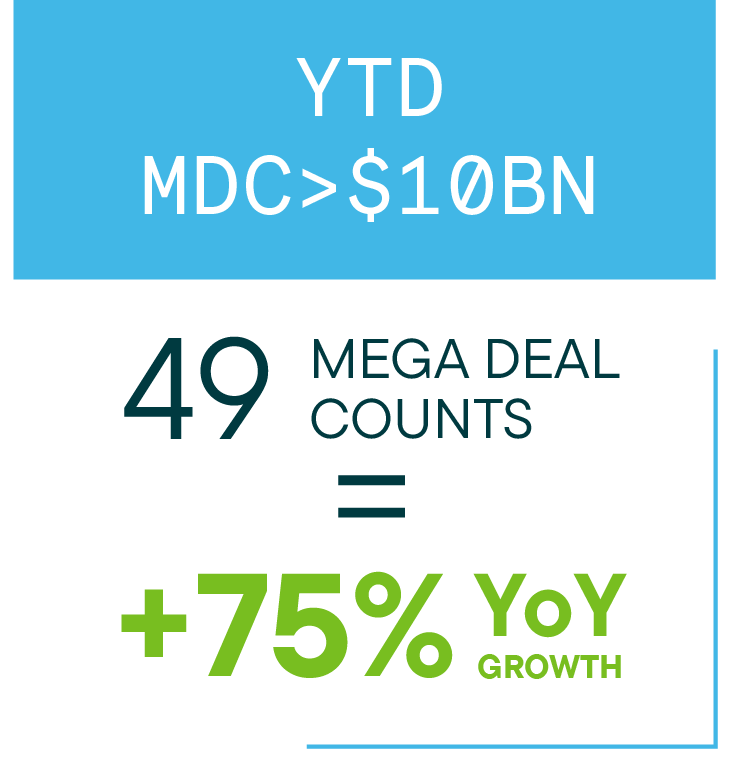

Quarter of the Mega-Deals: Global M&A Value Soars to 2nd-Highest Q3 on Record, While Deal Count Hits ~20 Year Low for Q3s.

Cross-border M&A is rebounding sharply, marking the biggest jump since 2021, as investors seek diversification away from U.S. listings amid rising geopolitical and regulatory risks.

Source: Reuters

IPO Trends

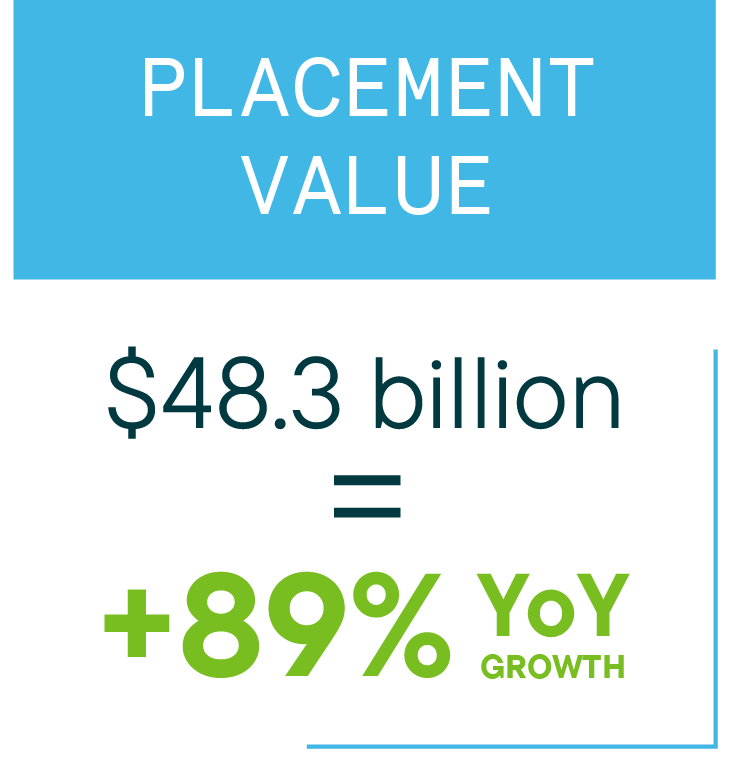

Q3 IPOs Extend 2025 Momentum: Global Deal Volume Rises Slightly While Placement Value Surges Above 2024 Levels.

Source: EY global ipo trends

AI Investment Trends

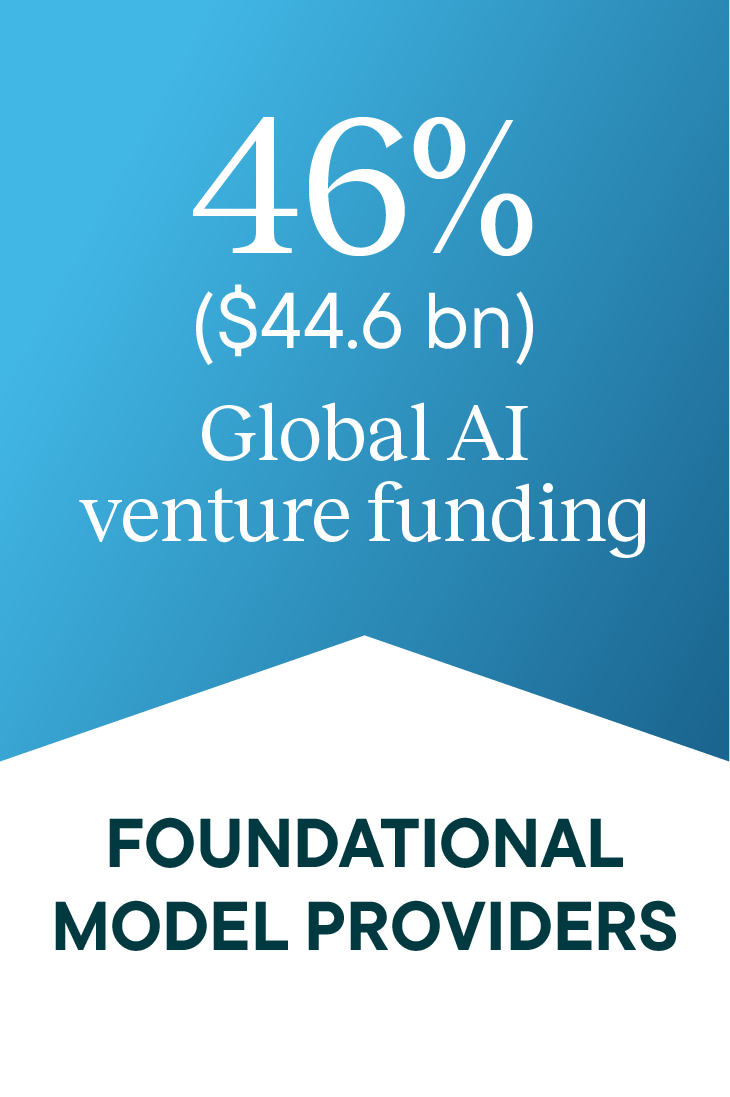

Although foundational model providers dominated the VC funding in Q3, we have observed a broad resurgence in Applied AI trends, with one notable example being the growing “space race” theme, where leaders such as ASTS and Starlink are adopting AI to optimize satellite constellations which intend to improve coverage and reduce latency.

Source: kpmg

AI Sector Concentration

sector

expansion:

Funding Concentration:

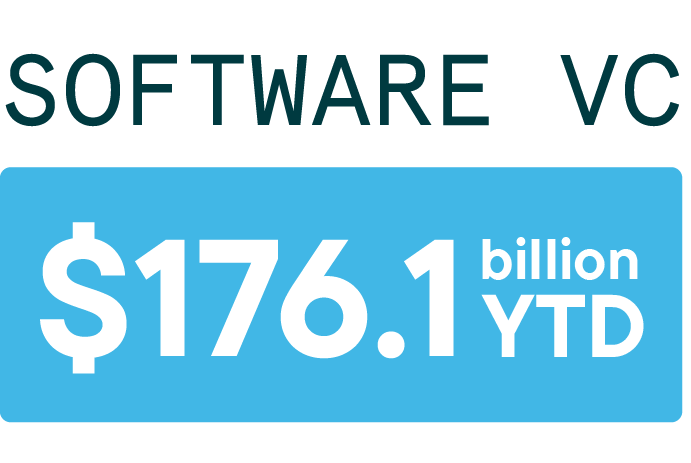

Applied AI, vertical SaaS, fintech, defense/space and healthtech.

Deep-tech areas like quantum computing and alternative energy.

software outlook:

The focus has shifted to scalability and strong defensible moats. Enterprise software is led by AI-native apps, infrastructure, and cloud security.

AI M&A Wave in Europe

100 M&A deals among European AI startups this year, fueled by the race to develop and commercialize AI.

key players:

AI Scaleups: well-funded startups like:

Mistral (FR): Raised €1.7B, now prioritizing M&A.

Domyn (IT): Seeking €1B; M&A is a "key part" of its strategy.

H Company (FR): Acquired Mithril Security after a $220M seed round.

European Sovereignty Issue:

Soaring AI valuations lure foreign buyers, but European Governments may slam the door (Intervention to keep strategic AI firms domestic complicates their exits).

Contractual / Governance Trends:

According to Q2 data (Cooley), investor-protective provisions such as pay-to-play and redemption clauses became more common, reflecting the cautious macro environment. By contrast, our observations at TheVentureCity suggest a more optimistic shift in Q3, marked by a greater prevalence of founder clawback clauses.

Source: cooley

Looking ahead

Just like the 19th-century railway boom, which triggered massive overinvestment but ultimately transformed economies, today’s AI surge could be the start of a similar long-term shift rather than a short-lived bubble.

At its peak, the 19th-century railway boom absorbed 20–30% of total U.S. capital formation, while current AI investment is estimated at under 1% of U.S. GDP, highlighting how much smaller today’s surge still is in relative terms.

As funds run low on liquidity and channel more capital into supporting overvalued portfolio companies, we could see a cooldown in new deal activity in the coming quarters.

We expect a growing share of available capital to be allocated to follow-on rounds, leaving significantly less room for new investments.

Ecosystem builder perspective

María Dancausa, product manager at TheVentureCity, describes our approach to building a GenAI product.

Rewind to this time last year, and the headlines were dark and ominous. They were ablaze with layoff news and economists fueling the fire with warnings of more turbulent times ahead. The questions on everyone’s mind: can the US pull off a soft landing while curbing inflation? How will quantitative tightening impact consumer spending? How will the technology ecosystem weather the storm?

A few things are clear in hindsight. In the public markets, investors enjoyed a strong end to the year, albeit after a bumpy start. The S&P ended 2023 at +24% and the tech-heavy Nasdaq at +43%. The magnificent seven, comprised of companies that already have some of the largest market cap, smashed it with a 111% YoY growth (Kiplinger). Within this power basket is NVIDIA, the stock everyone wishes they had bought in Q1 2023, which ended up an astonishing 239% over the full year of 2024 (Statista).

Last quarter we reported a brief opening of the IPO market. We remain confident that we will see more companies go public in the back half of 2024 and into 2025, and have noted hundreds of quality candidates detailed in CB Insights’ IPO pipeline of 250+ companies (CB Insights).

Bucking the downward B2C trend we mentioned earlier, Shopify, up 124% YoY, caught our attention. We have always leaned into the e-commerce enabler space, making notable investments such as in our very own Returnly, acquired by Affirm in 2021, so we are excited to see the momentum within this space.