TRY OUR GROWTH SCANNER

Venture Capital Benchmark Q2 2025

US, Europe, and Latin America

As we've done for years, we're back with a fresh take on how founders are crafting their funding strategies and investors are deploying their capital in the startup and scaleup world. This time, we're offering founders, investors, and ecosystem players a new lens for reading the data. While most of what we share is grounded in facts and objectivity, you know us… We couldn’t resist adding a splash of color, a few strong opinions, and even a bit of a challenge.

%20(3000%20x%201100%20px)-2.svg)

Funding Frenzy: How VC Dollars Flowed This Quarter (US, LATAM, Europe)

Key Takeaways

Global venture funding hit $115B in Q2 2025, jumping 29% from Q4 2024's $89B, but here's the twist: deal counts dropped 29% from Q1's 8,500 to just 6,000 transactions, pushing average deal sizes to a hefty $19.2M across all stages according to Pitchbook data. What we're seeing is a pretty stark split in the market where massive rounds are driving the big numbers while the actual number of deals keeps shrinking. We are seeing that founders bootstrap more, and ask for capital later when they already have validated their Tech. Also AI AI-driven companies are very capital intensive mid and long term. More efficient in capital to validate all first but as they grow they need big money to stay relevant.

This surge is largely thanks to AI's continued dominance, with quarterly funding growing 145% from Q3 2023's $47B baseline to today's record levels. Companies with distinctive AI capabilities grabbed over 71% of all the money deployed this quarter, showing just how concentrated AI investments have become across every sector. If current H1 momentum continues, 2025 could hit around $450B in combined regional funding, potentially matching 2021's historic levels despite transaction volumes heading toward just 15,000 deals, the lowest we've seen since before 2020. AI is eating the world. Funny to think that we won't be talking about it in a couple of years once everything is AI embedded…

%20Q2%202025.svg)

Geography-wise, the concentration has gotten even more intense, with Bay Area companies scooping up huge chunks of that $115B quarterly deployment. European markets have shown strong resilience, keeping funding steady in the $13-17B quarterly range, while LATAM has demonstrated significant volatility, swinging wildly from $3.5B to $1.05B between quarters. All of this is happening alongside major shifts in the secondary market and faster exits, painting a picture of significant structural changes toward late-stage consolidation across all the major venture ecosystems.

Fundraising by Geography

US

Q2 2025 shows a mixed picture for US venture capital. Capital invested hit $100B, up 14% from Q1's $88B, while deal count dropped 24% to around 3,700, marking the seventh straight quarter of decline. This gap pushed average deal size to a record $27M, reflecting continued momentum in AI and late-stage consolidation that built on 2024's recovery from $31B in Q4 2023 to $71B in Q4 2024.

Extension rounds rose to 28.1% with shorter 21-month fundraising cycles as capital gets deployed more selectively despite plenty of dry powder sitting around. The market shows clear division: record funding levels going to proven late-stage companies, while early-stage deal activity keeps shrinking as investors favor performance over speculative bets, with deal volume down 45% from Q1 2024's peak of 6,700 transactions.

EU

Q2 2025 shows European venture capital staying selective despite ongoing challenges. Capital invested reached $13.5B, down 15% from Q1's $15.8B but still above 2023 lows, while deal count dropped 35% to around 2,200 deals, marking the steepest quarterly drop since Q1 2024's peak of 5,300 transactions. Average deal size jumped to $6.1M, showing how the market has consolidated toward fewer but larger investments.

The region's funding has stayed fairly steady at around $13-17B since 2023, demonstrating stability while the US has seen more dramatic growth from $31B to $100B over the same period. With deal counts at multi-year lows and funding getting more concentrated, the European market mirrors the US trend of favoring proven late-stage companies over early-stage ventures, with investors on both sides of the Atlantic becoming more selective and focusing on performance over riskier bets.

This is when, if Europe had the right mindset, it would be the best time to invest. Rather than maintaining stability, this is the moment to place the big bets in Tech.

LATAM

Q2 2025 highlights Latin America's rollercoaster venture market. After Q1's record $3.5B surge, capital invested crashed 70% to $1.05B while deal count dropped 29% to around 220 deals. The Q1 spike was likely driven by a few mega-deals before things settled back down, though average deal size stayed strong at $4.8M, well above the usual $0.9M-$1.7M quarterly range since 2023.

LATAM represents 1% of global VC funding but shows promising signs of growth and investor interest. The market remains dynamic with natural fluctuations as the ecosystem develops, and while deal activity is down 59% from 2024 peaks, bigger deal sizes demonstrate growing investor confidence in the region. The market's responsiveness to large deals reflects strong investor appetite and the potential for significant impact from individual investments in this developing ecosystem.

Key learnings we are sharing

From Pause to Pivot: How Secondary Markets Are Powering Liquidity

Secondary markets have become the primary liquidity mechanism as traditional exits remain constrained. The secondary market is projected to handle $122 billion in assets in 2025, yet secondaries still account for just 1.9% of total unicorn value, revealing massive untapped potential worth $6+ trillion.

A critical shift occurred in Q1 2025: secondary transactions traded at premiums (6% average, 3% median) for the first time since 2022. However, this premium environment is bifurcated, elite startups command premiums while lesser-known companies face 30-60% discounts from their last valuations. This creates a two-tier market where quality determines pricing power.

The most telling metric: TVPI figures showed first positive momentum in years across 2017, 2018, and 2020 vintages after five consecutive quarters of decline. This uptick coincides directly with increased secondary activity, revealing that funds are using secondary sales to artificially stabilize portfolio valuations. Fund managers strategically time sales during years 5-7 of investments, the optimal window when portfolio growth slows but before traditional exits materialize. At TheVentureCity, we have made two secondary transactions this year, Before.ai without a discount, and Tucuvi.ai with a 20% discount. We're also actively exploring secondary market opportunities for our first F&F vehicle, 2016 and First Series A Fund vintage 2017 to provide liquidity to our existing LPs, adapting to these market dynamics where traditional exit paths remain limited.

With $1.1 trillion of unrealized NAV trapped in 2016+ vintage funds, secondary markets have evolved into fund lifecycle management tools. GP-led continuation funds extend fund lives instead of distributing capital, while LP-led secondaries offer better buyer-seller alignment, fundamentally altering VC return profiles. The result: secondary markets nearly equal private equity secondary scale but operate in an opaque, concentrated environment where pricing discovery remains limited to elite companies.

How Tariffs Are Reshaping VC Markets: From Global to Regional

Rising tariffs are fundamentally reshaping venture capital into a regional game, disrupting the global investment landscape that defined the past decade. With average US tariff rates jumping from 2.5% to 27% in early 2025, cross-border operations face mounting challenges while global supply chains become major risk factors, forcing VC firms to become increasingly cautious and concentrate on sectors like AI with clear growth potential and tariff-resistant business models.

This disruption presents a strategic opportunity for Europe after years of losing ground to US tech dominance. While Europe's share of global VC funding dropped from 16% to 11% in Q1 2025, the forced regionalization could reverse this trend as European startups pivot toward EU partnerships and domestic manufacturing alternatives. The software and AI industries, though not directly targeted by tariffs, face indirect pressures from rising hardware costs and reduced IT budgets as global trade environments shift.

The talent migration is particularly striking in tech, with Europe actively recruiting skilled workers back from the US as cross-border mobility becomes more complex. Defense tech and deep tech sectors are emerging as winners, attracting investors betting on domestically-oriented, tariff-resistant businesses. For Europe, this regionalization represents a chance to reverse brain drain and build stronger internal capabilities, but success will require companies to implement strategic risk management and navigate evolving trade regulations amid growing geopolitical tensions.

There's one thing tariffs can't touch: mindset. You're either wired for limitless thinking and global ambition or you're not. No matter how much capital is raised or how much talent is attracted, without the right mindset, Europe will continue to trail behind the US when it comes to risk-taking and scale-driven vision. European investors, in particular, need a mentality shift—too often, they're still thinking in terms of local markets rather than global domination, favoring incremental growth over exponential scaling

That said, the tides are shifting. Ultra-talented individuals from emerging markets—many of whom once looked exclusively to the US are now choosing Europe as their launchpad. It’s an exciting moment. But to truly lead, Europe must evolve its mindset to match its growing potential.

The Healthcare AI Revolution: How Startups Are Redefining Medical Innovation Economics

Healthcare AI has completely reshuffled the venture capital deck, grabbing nearly 30% of all healthcare investment in 2024, and 2025 it's heading down the same path. These tech-savvy startups are simply outperforming everyone else, they're growing revenue faster and locking in multi-year contracts at rates that make traditional healthcare software companies look sluggish. Amazing to watch how timing has its effects. Two years ago, this was unthinkable…

The numbers tell the story: healthcare tech pulled in $5.6 billion in 2024, nearly tripling from the year before. Meanwhile, fintech has been bleeding money, dropping from $120.8 billion in 2021 to just $43.3 billion now. Healthcare startups are also racing to unicorn status faster than anyone expected. Take Abridge, which took approximately 4 months to climb from the $2.75 billion mark to a $5.3 billion valuation, that kind of speed used to be impossible. And it's not just the later-stage players; earlier-stage companies like Spikeapi.com (raising $3.5M in Seed funding) and TonicApp.io (€6M Series A) show strong growth and potential of how deep this opportunity goes.

Clinical documentation (Some would say one of the greatest pains in the a**) has become the real money-maker, with automated tools keeping customers happy in ways that older software never could. Here's the kicker: if you can integrate with Epic's EHR system in the US, you're basically printing money. Companies that nail that integration see both funding and sales take off, making it the closest thing to a guaranteed win in healthcare tech.

Deeptech & Deep Europe push

Europe's deeptech scene is finally hitting its stride after years of untapped potential. The continent has always been a research powerhouse, with universities consistently ranking among global leaders in scientific output. But for too long, there's been this frustrating gap between brilliant lab discoveries and profitable companies. European deeptech startups used to get stuck in that research-to-market gap. These companies need longer timelines than your typical app startup, require large amounts of capital, and have to navigate regulatory frameworks that move pretty slowly. While a software company can pivot over a weekend, quantum computing startups need years just to prove their basic concept works.

But things are looking way better now, and the timing couldn't be more perfect. Both money and policy are finally catching up to Europe's scientific edge. Government programs like the European Innovation Council's €10 billion fund are stepping up with patient capital that actually gets how deeptech works, while corporate giants like Siemens, SAP, and Airbus are actively hunting for breakthrough technologies. A whole new wave of specialized deeptech VCs actually understand that you can't rush quantum sensors and fusion reactors like you would a mobile app. These funds, backed by investors with a long-term horizon, are laying the groundwork for the next wave of transformative innovation.

The current tariff situation and push for tech independence are making things even more interesting. European governments are suddenly very motivated to cut dependence on foreign technology, driving serious investment into autonomous systems, cybersecurity, and advanced manufacturing. Plus, the green transition is creating huge demand for everything from next-gen batteries to carbon capture tech. For the first time in ages, being a European deeptech startup feels like a real competitive advantage—you've got patient European capital meeting urgent European needs, and that's a pretty sweet spot to be in.

US Market Fund Performance

US venture fund performance tells a pretty clear story about timing and market cycles. The 2017 vintage really nailed it with a median TVPI of 1.72x and solid distribution activity (0.26x median DPI), while the best performers hit 4.22x TVPI. Performance gets progressively weaker through the next few years, with 2018-2020 funds showing declining median TVPIs from 1.38x to 1.08x as market conditions got more expensive and competitive. The 2021-2024 vintages are still early in their lifecycle, with median TVPIs around 1.0x as portfolio companies continue to develop and mature, highlighting how market timing and disciplined deployment remain key factors in long-term venture performance.

Within these market dynamics, TheVentureCity's fund performance demonstrates solid execution. TVC Fund I (2017 vintage) shows a DPI of 0.35x and TVPI of 1.65x, performing close to the median for that strong vintage year. Our Opportunity Fund I (2020 vintage) has achieved a TVPI of 3.03x, significantly outperforming the 1.08x median for that vintage, while Genus Ventures, our initial F&F vehicle, has already delivered a DPI of 1.15x. These numbers are particularly promising considering that several portfolio companies with significant potential, including RecargaPay and Simpliroute, have yet to exit, creating additional upside potential across our fund performance metrics.

Looking Ahead – The Watchlist

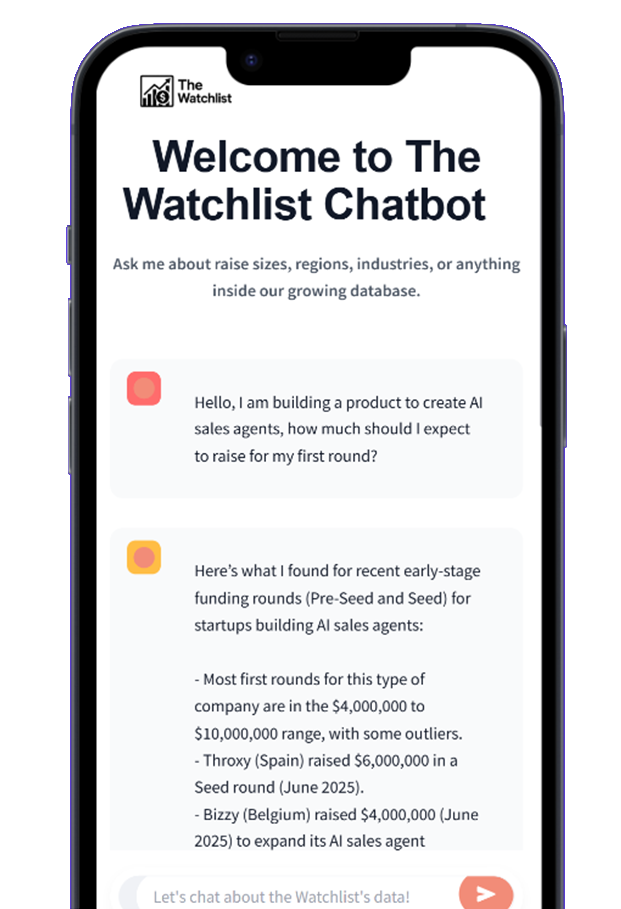

As the venture landscape evolves—with increasing geographic diversity, mega-round concentration, and AI-driven investment shifts—access to real-time, comprehensive market intelligence has never been more critical. The Watchlist, developed internally at TheVentureCity and now in beta, delivers timely insights on early-stage funding across Europe, LATAM, and North America so you can stay ahead of the curve.

More than a database, The Watchlist features an AI-powered chatbot that lets you converse directly with our funding-round dataset. Ask about industry trends, drill into regional patterns, or uncover hidden opportunities—our assistant provides personalized guidance in seconds.

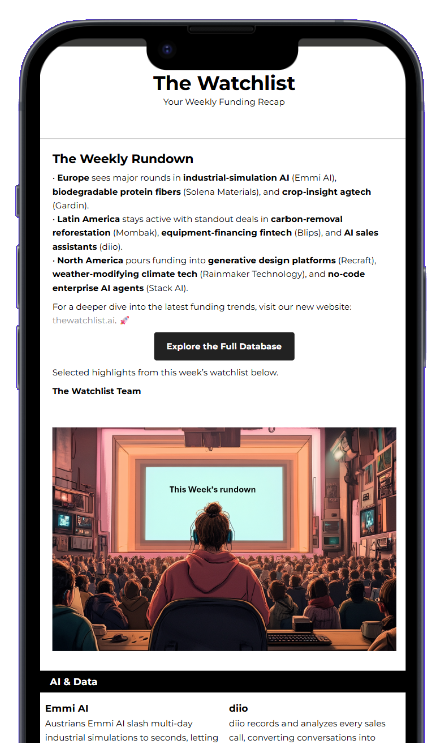

Every week, subscribers also receive an exclusive, visually engaging newsletter packed with curated highlights that cut through fragmented information. Whether you’re sourcing deals, benchmarking your startup’s growth, or scouting strategic partnerships, The Watchlist gives you the critical insights to act faster and smarter.

Don’t miss out on the future of venture intelligence. Subscribe during our free beta to unlock full database access, start chatting with our AI assistant, and receive your weekly funding brief—delivered straight to your inbox.

🔔 Subscribe Now

🌐 Discover More → thewatchlist.ai

💬 Start Chatting → chat.thewatchlist.ai